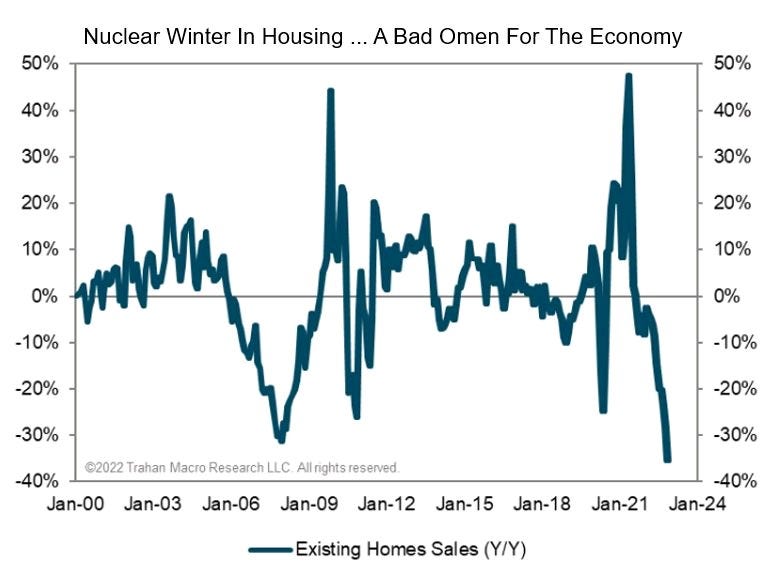

"Nuclear winter" for US housing

"Nuclear winter" for US housing

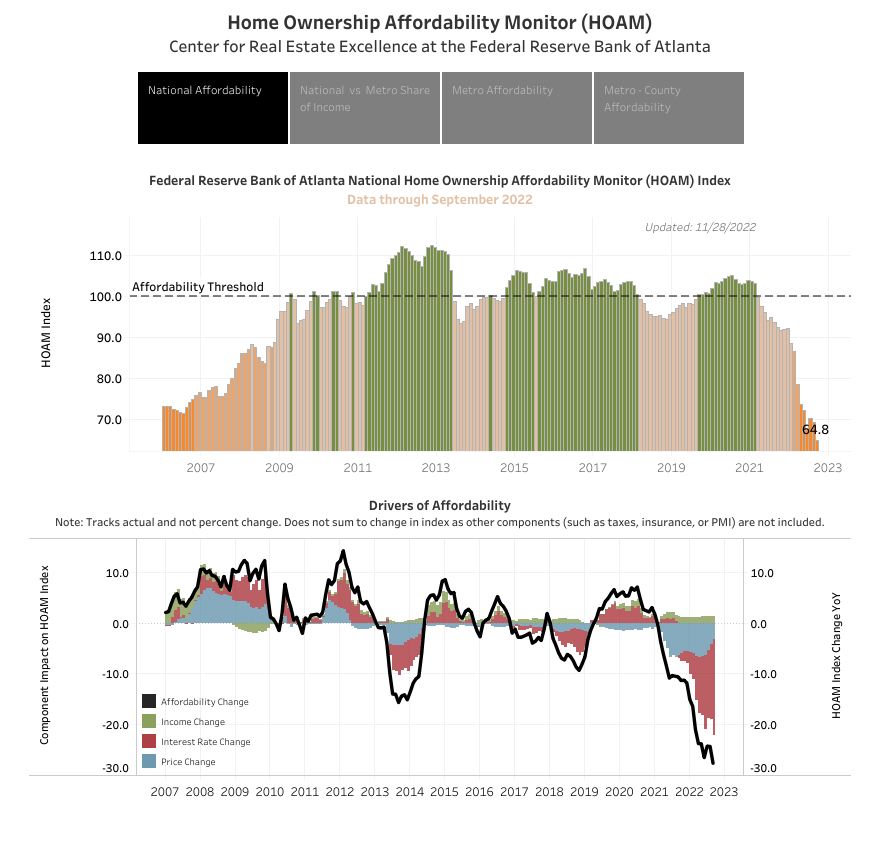

Affordability worst in years

The US housing market is falling apart.

Yet, many industry experts failed to see this coming. As recently as October 22, 2021 (source: CNN), real estate executives were quite optimistic about the future:

“The impact of…higher rates shouldn’t be a source of major concern for the housing market.” — JPMorgan Chase chief financial officer Jeremy Barnum

“Residential is still pretty hot. Remodeling activity is good. Housing starts are good. I don’t see any real negatives in the future. No storm clouds on the horizon, I would say, from our viewpoint.” — Mark Sheahan, CEO of Graco, which makes paint sprayers for home owners and contractors

“Housing remained well below historical and structurally needed levels for over a decade. This is compounded by pent-up demand from millennials that we’re only now beginning to see.” Also, “interest rates remain at historically low levels” and “the housing market…will be a strength.” — Whirlpool CEO Marc Robert Bitzer

Today - just 14 months after the above statements were made - data is illustrating that the US housing market is in its worst shape in decades.

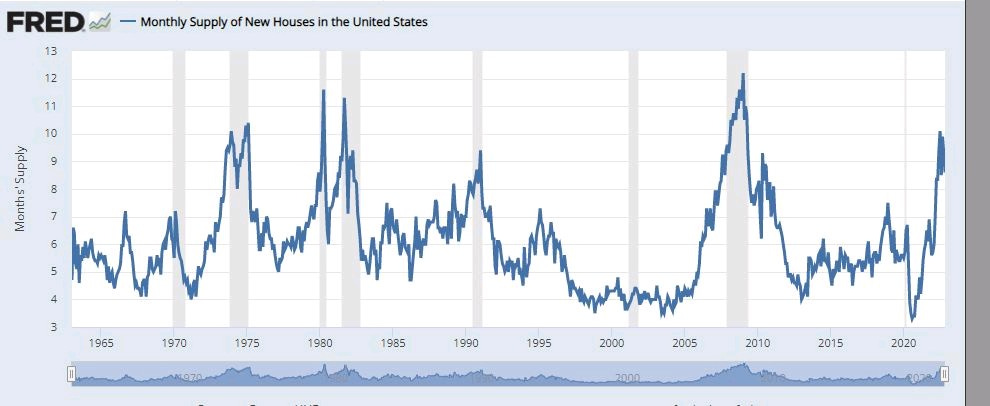

Affordability - driven by prices and debt servicing costs - has plummetted to levels lower than leading up to the Global Financial Crisis. Volumes have also tanked, causing inventories to pile up.

While housing bear markets don’t always lead to financial crises, most drag the broader economy through the mud for a couple years. Housing sales volume is closely related to many other economic activities, such as construction, lending and durable goods purchases. When housing activity declines, the fallout is widespread.

Also, housing bear markets tend to last a long time (because real estate is a less liquid, less efficient market), so price discovery and adjustment can be long and painful. Finally, shrinking home equity levels tend to erode the consumer’s willingness to spend on discretionary items.

Despite this, many Wall Street (and Bay Street) economists are still forecasting a mild recession sometime in 2023, along with positive equity markets. These predictions mainly depend on an indisputable decline in inflation, after which the Fed will ease up on rates.

A mild recession would coincide with a gradual moderation of inflation towards more acceptable levels (2% is what Powell is still saying), and we’re already running out of time for this to become reality in 2023. Inflation could fall faster, but that would be more aligned to a hard-landing scenario. The longer rates remain high, the more likely the economy nosedives. Unfortunately, nobody knows how long is “too long”.

Right now the engines are out, the plane is gliding and we’re all wondering how we reach the ground.