Should parents pay for college?

Should parents pay for college?

Easy for some. Not for most. Here's what you should consider.

If a caring friend forwarded this to you, please subscribe:

A friend of mine (let’s call her ‘Jane’) recently brought up the cost of putting her children through college. It turned out she was paying all the bills.

This would be great if she could afford it.

But she can’t.

Jane is 51 years old and earns roughly $90,000 per year. She will likely happily work for another 15 years. Currently she has about $400,000 in retirement savings and plans to aggressively save during her remaining working years.

To help her children pay for college, she has withdrawn some of her savings and tapped into a line of credit.

As a parent, I can understand the instinct to do everything you can for your children. However, I don’t believe parents should put their retirement at risk to pay for their kids’ education.

I realize I’ve probably ticked off a few people.

What is the parental obligation?

The moral argument that parents are obligated to provide an education for their children is strong. I agree that people shouldn’t have kids if they’re not willing to set them up for the world. However, what that means has evolved over the decades. Today that might mean a masters degree. But what were parental obligations 50 years ago? And what will they be 50 years from now?

The parental obligation seems to have grown over the years. Regardless, parents with college aged children today should have known what they were getting into, but at what point does the obligation end? Maybe never. I don’t know.

Of course, the decision is more than moral. It’s pragmatic. Money doesn’t appear out of thin air, and for that reason there are many additional considerations.

Who’s paying for retirement then?

Let’s put the moral argument to the side.

There is a pressing financial issue facing parents today. The cost of post-secondary education continues to rise faster than incomes. While it is increasingly necessary to get a college education, it is also increasingly financially unattainable for many people.

This is happening while much of the world faces a retirement crisis. People simply have not saved for retirement. Jane is one of the lucky ones, yet she still faces a shortfall if she doesn’t continue to aggressively save and invest.

Jane’s ability to fund her retirement is at odds with her desire to pay for her children’s education. She probably cannot do both.

Her window of opportunity to remain self-sufficient in retirement is closing. The more she financially commits to her children’s education the less likely she will retire as planned. Of course, plans have a way of going wrong anyway. Any number of unexpected events - ill health, redundancy - can cut her timeline to retirement in half. Jane has limited time and lots of downside risk.

In contrast, her children will have 60 years ahead of them once they graduate from college. If they pay for their own education, this is plenty of time to repay debts. If they pursue the right career path, they likely have much more upside than Jane has downside. Moreover, if Jane’s retirement is adequately financed she will retain independence. If Jane sacrifices her retirement to pay for her children’s education she will invariable depend on them (perhaps even live with them) once she stops working. Whether this is good or bad is up to the family to decide, but you must recognize that each option comes with trade-offs.

The biggest trade-off for Jane’s kids if they self-fund their education is they will be saddled with debt on day 1 of their working lives. That seriously restricts their ability to take entrepreneurial risk. It also forces them to take the first job that comes their way, perhaps sending them down a path they didn’t envision. Debt is restrictive and stifling.

As you can see there are no clear cut answers (unless you’re rich), but here is what I think:

The decision to go to college and pursue a stream must be carefully evaluated. College is simply too expensive to use as a place to find yourself. Students (and parents) must have a path in mind and need to fully understand the return on investment of a college degree.

Education costs should be shared by both parents and children. Everyone needs a stake in the game. Not only does this reduce the burden, I believe it builds commitment. The more a student is aware of the difficulty in paying for college, the harder they’ll work to get the most out of their education.

Avoid paying for college using debt. If any debt must be incurred, the child should borrow (not the parent). The downside risk for a middle-income, middle-aged parent struggling to save for retirement is simply too large.

Prepare well in advance. In anticipation of college costs (even if the child is still a toddler) cut some expenses. Forgo a trip or two. Importantly, the child must participate in these sacrifices starting at an early age. And when they can get a part time job, a significant portion of their earnings should be stashed away for school.

I don’t have all the answers, but I hope I have provoked some discussion. Please comment to share your thoughts!

Also of interest:

DumbWealth categories:

Wealth * ETFs * Work * Real Estate * Master Class (NEW) * Income Investing

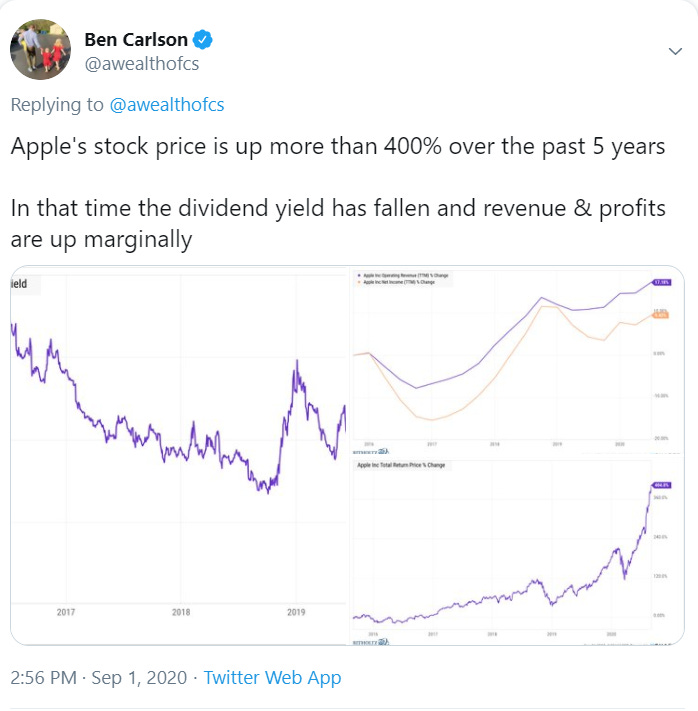

Tweet of the week:

By @awealthofcs

Here are the charts that were embedded in his first tweet:

Legal

DumbWealth.com and its email communications contains information, data, documents, pages and images (“the Information”). While the Information is considered to be true and correct at the date of publication, changes in circumstances after the time of publication may impact on the accuracy of the Information. The Information may change without notice and DumbWealth is not in any way liable for the accuracy of any information printed and stored or in any way interpreted and used by a user.

The Information is made available on the understanding that DumbWealth and its employees and agents shall have no liability (including liability by reason of negligence) to the users for any loss, damage, cost or expense incurred or arising by reason of any person using or relying on the information and whether caused by reason of any error, negligent act, omission or misrepresentation in the Information or otherwise.

DumbWealth is not a registered financial advisor. All Information provided is for entertainment and educational purposes and is not an investment recommendation. Before making any investing or personal finance decision, please consult a registered financial advisor.