T-Bills are Sexy Again

T-Bills are Sexy Again

What a difference a year makes

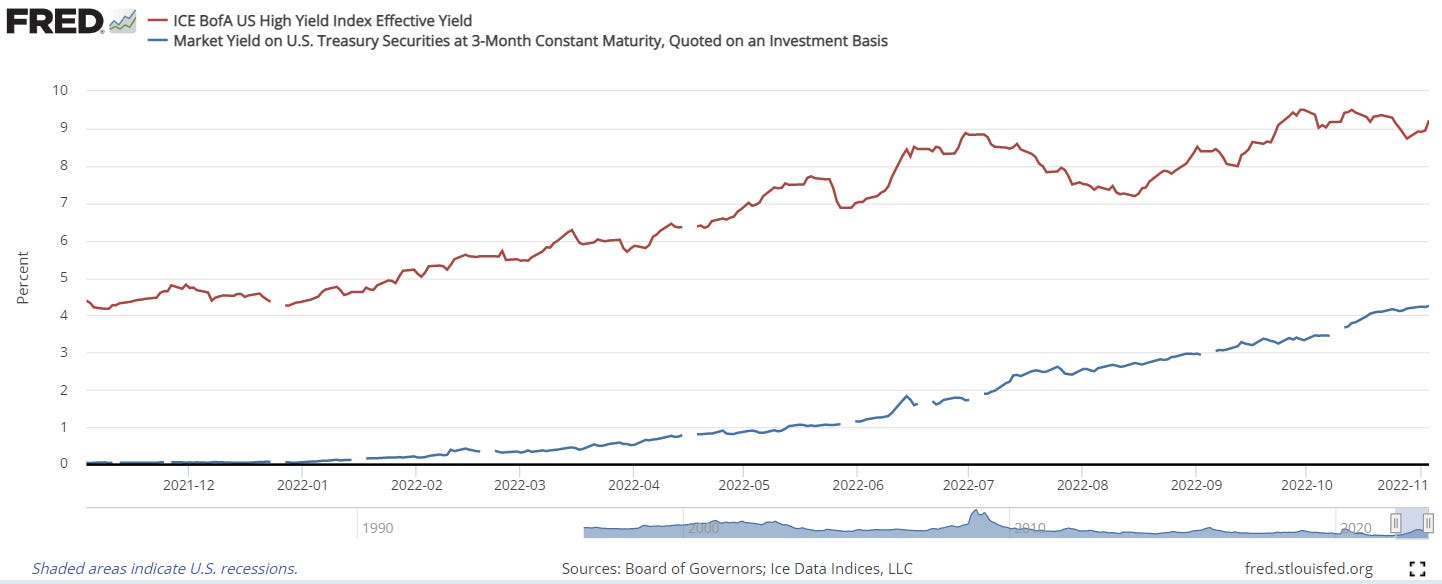

1: The 2 year US Treasury yield at 4.71% is HIGHER than high yield bond yields at the beginning of 2022!

Want to go shorter duration? 3 month T-bills are yielding (4.12%) essentially what HY provided on November 9th, 2021 (4.17%). T-bills are sexy again!

Compare those yields on risk-free securities to the S&P 500 earnings yield of about 5% and dividend yield of 1.73%.

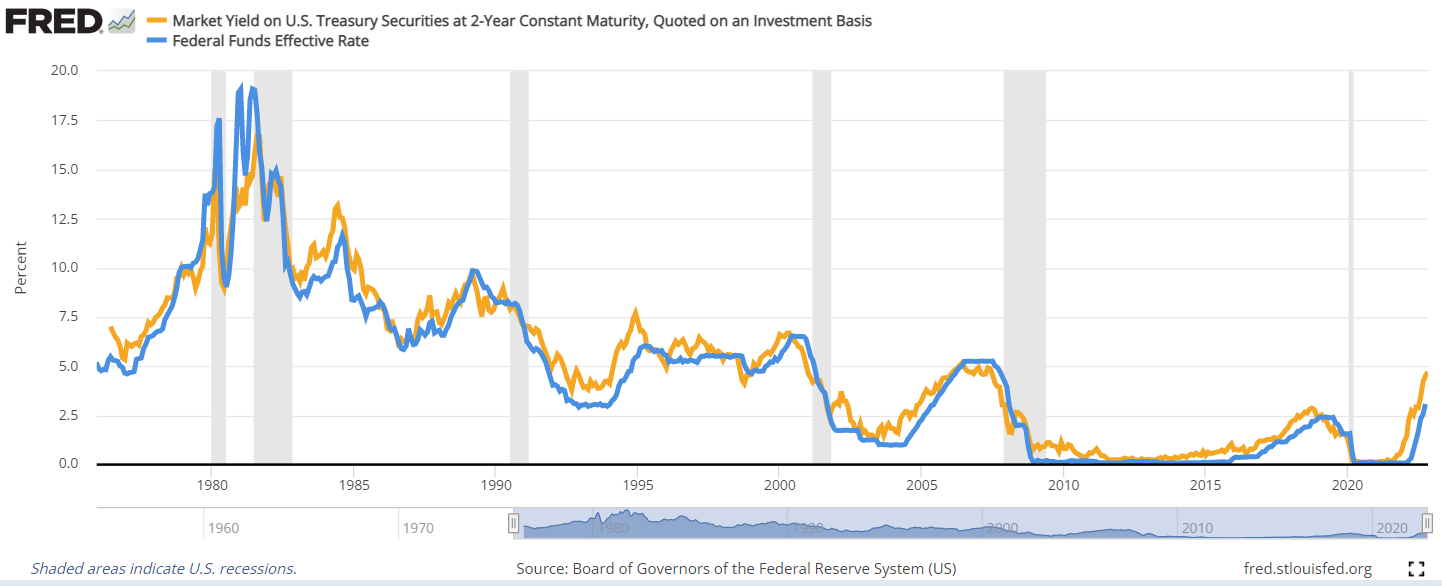

2: When will the Fed pivot? Watch the 2yr US Treasury yield.

The chart below shows how the 2yr tends to lead the effective fed funds rate. I wouldn’t solely rely on this indicator, but it should definitely be part of your arsenal in determining policy moves.

With that said, everyone is so focused on the pivot - I wonder what people expect to happen when rates pause or start to decline. Experience shows that yields peak and begin to fall because something is broken.

By the time the Fed starts lowering rates, the downward economic and financial momentum might have taken on a life of its own. The Fed is still fighting an 8.2% CPI (looking through the rear-view mirror), while liquidity has evaporated, housing is collapsing, energy prices are elevated and the consumer is stretched. The economic momentum is already negative and the rate hiking cycle isn’t even done.

Don’t let jobs data fool you into thinking things are rosy - employment is a lagging indicator. If anything, strong jobs reports give the Fed cover for hiking even more.

Powell continues to push against core PCE, restating his commitment to a 2% target. If inflation does begin to decline - and many indicators (e.g. breakeven yields) suggest this will happen - while the Fed continues to run tight monetary policy, the risk is inflation overshoots to the downside. Like I’ve said before, we might be talking about deflation sometime in the next 12 months. This is what the pivot may be fighting - a situation not beneficial for risk assets.

Of course, there is a chance we get the goldilocks scenario where inflation comes down gently, housing prices bottom, Powell eases up before overshooting and markets rally hard. Maybe, maybe not.

This is what makes macro forecasting hard. You can’t simply make a six month prediction and walk away. Your view of the future needs to be reconciled against each piece of information that comes out daily. This is the why I write this online ‘journal’. It’s a way to make sense of the data hitting me from all directions while interacting with likeminded people.

Thanks for reading!