Where did all the workers go?

Where did all the workers go?

Charts for the visual analyst

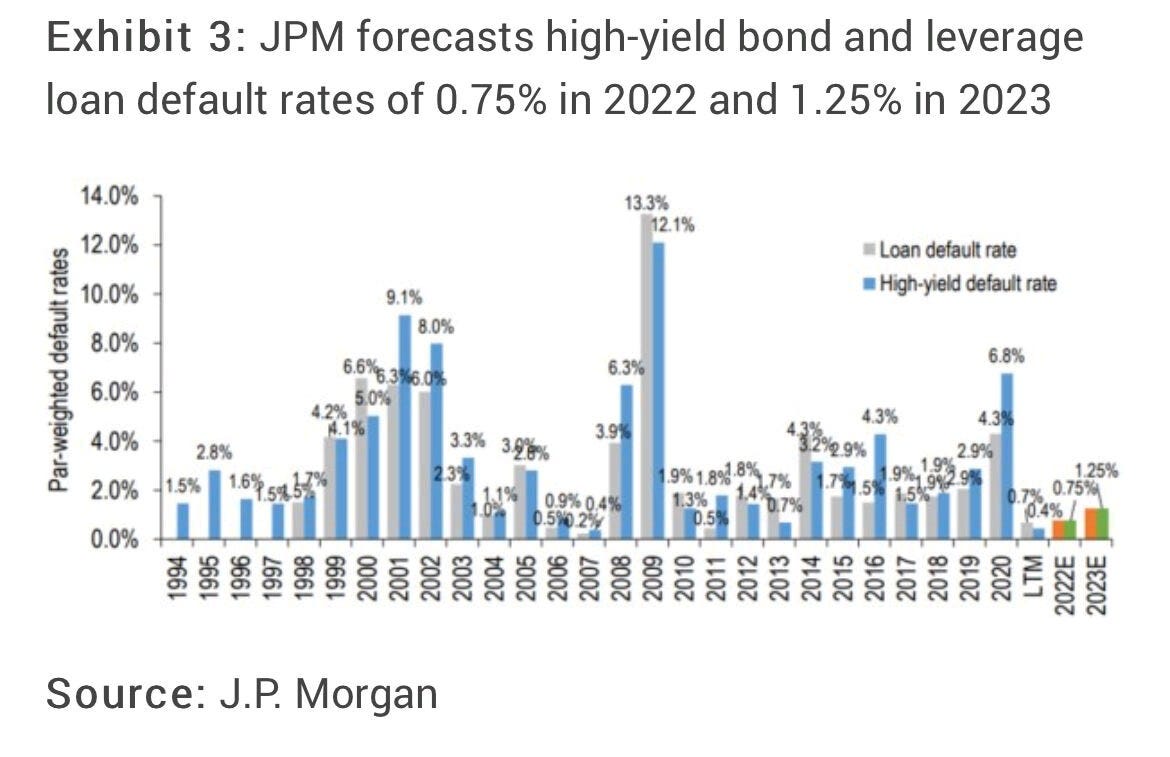

Fact 1: Leveraged loan default rates are expected to remain very low over the next couple years, according to JP Morgan, providing some foundational strength to risk assets overall.

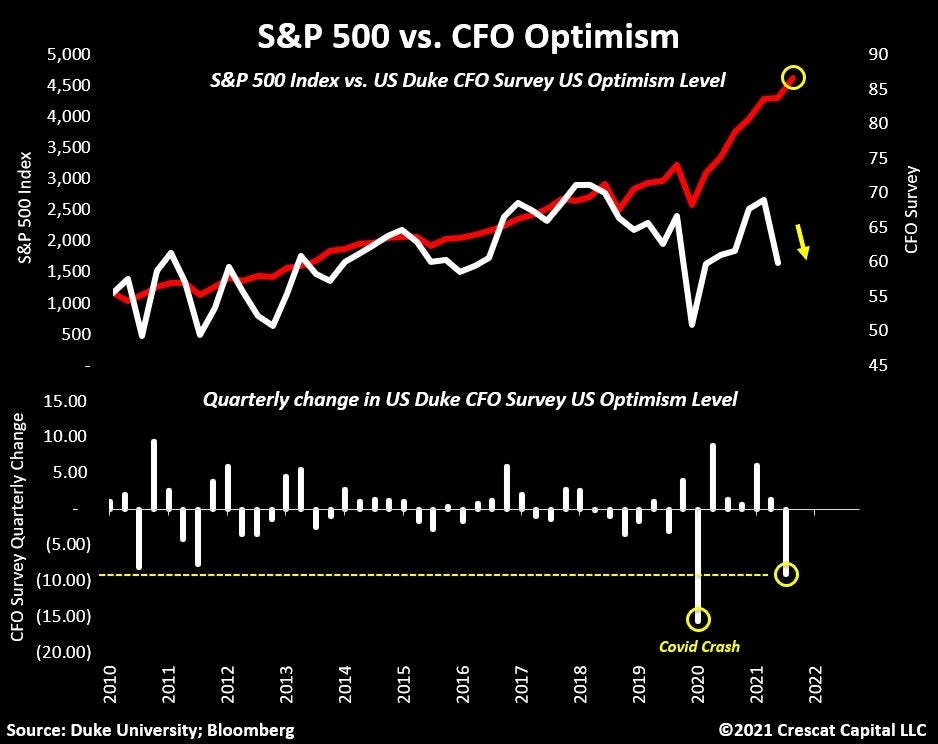

Fact 2: Despite low expected default rates, CFO optimism has ticked down. I wouldn’t necessarily read too much into this change in sentiment, as it might simply be a reversal of over-optimism coming out of the Covid recession. Regardless, this is worthy of note given the size of decline.

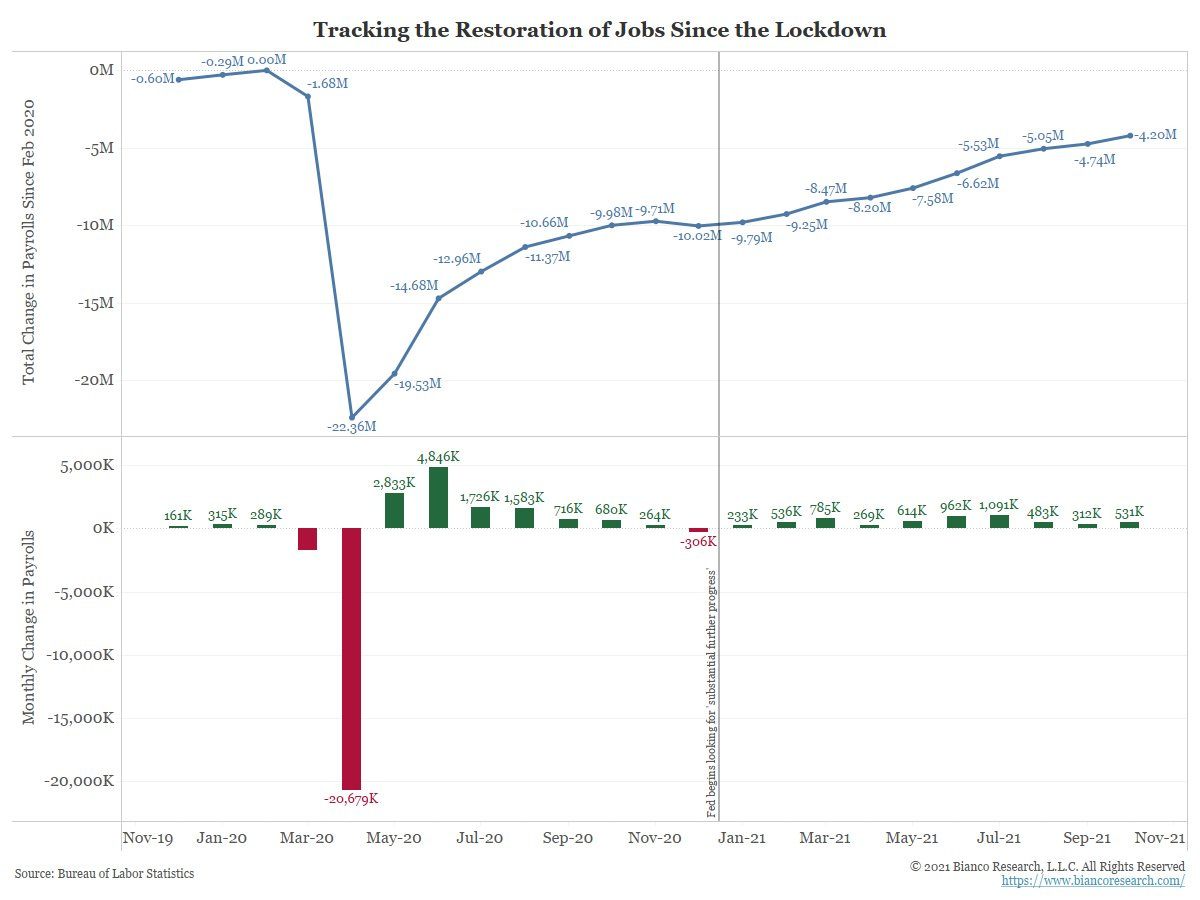

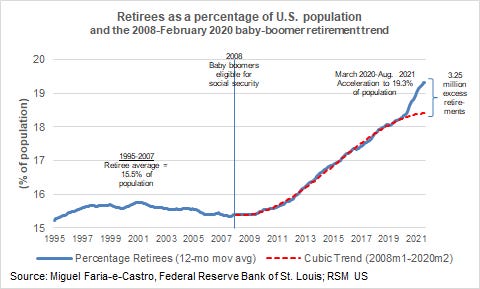

Fact 3: Despite the unemployment rate falling to 4.6% in October, the number of people employed in America is still 4+ million below the pre-covid peak. In other words, the labour participation rate has plummeted and people are not returning to the workforce. The labour participation rate in the US remains about 2% below pre-Covid levels (this is significant).

Where did workers go? The second chart shows that 3.25 million workers have decided to retire earlier than expected, explaining a big part of the employment variance. These unexpected early retirements are pressuring labour supply.

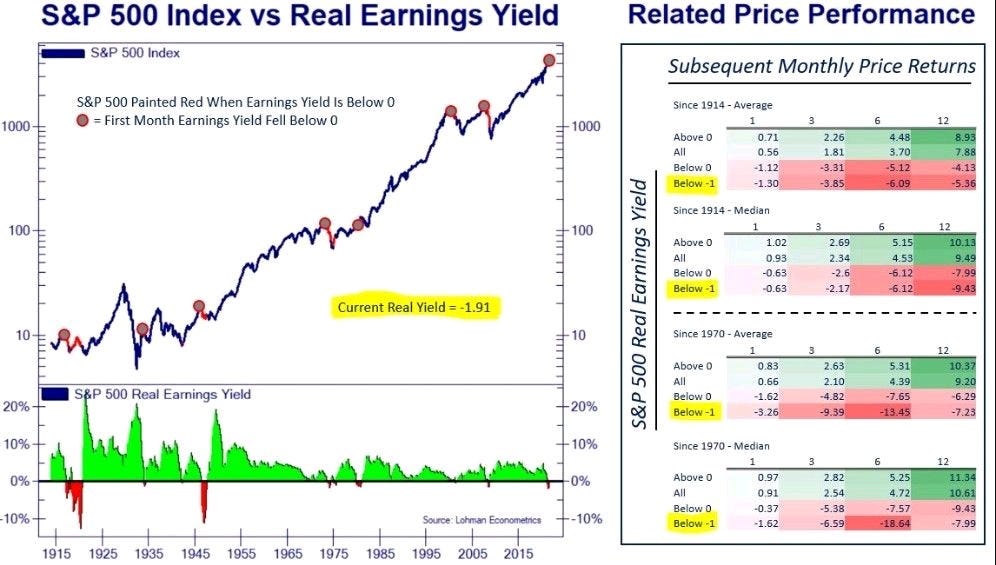

Fact 4: According to Lohman Econometrics, the real earnings yield for the S&P 500 is -1.91%. Historically, when real yields fell below 0, subsequent 1yr stock market returns were not good. Note the important exception, however. In 1929 the real earnings yield was decidedly positive…right before the market crashed.