Are things going to get worse?

Are things going to get worse?

Market stress and recession talk

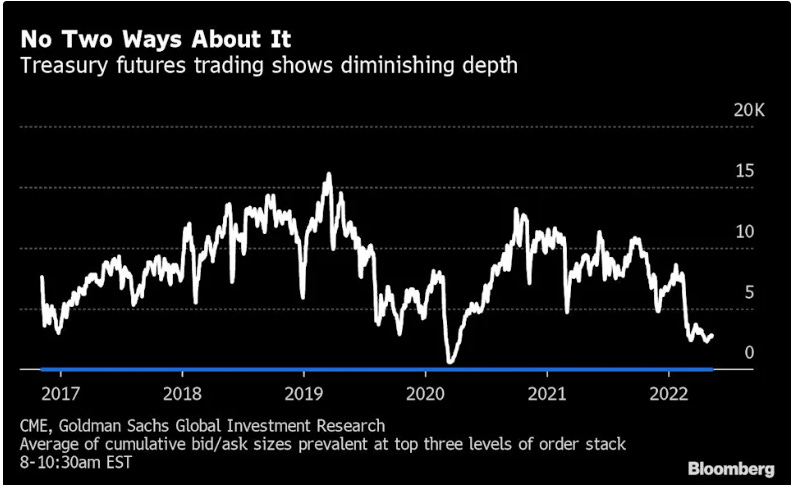

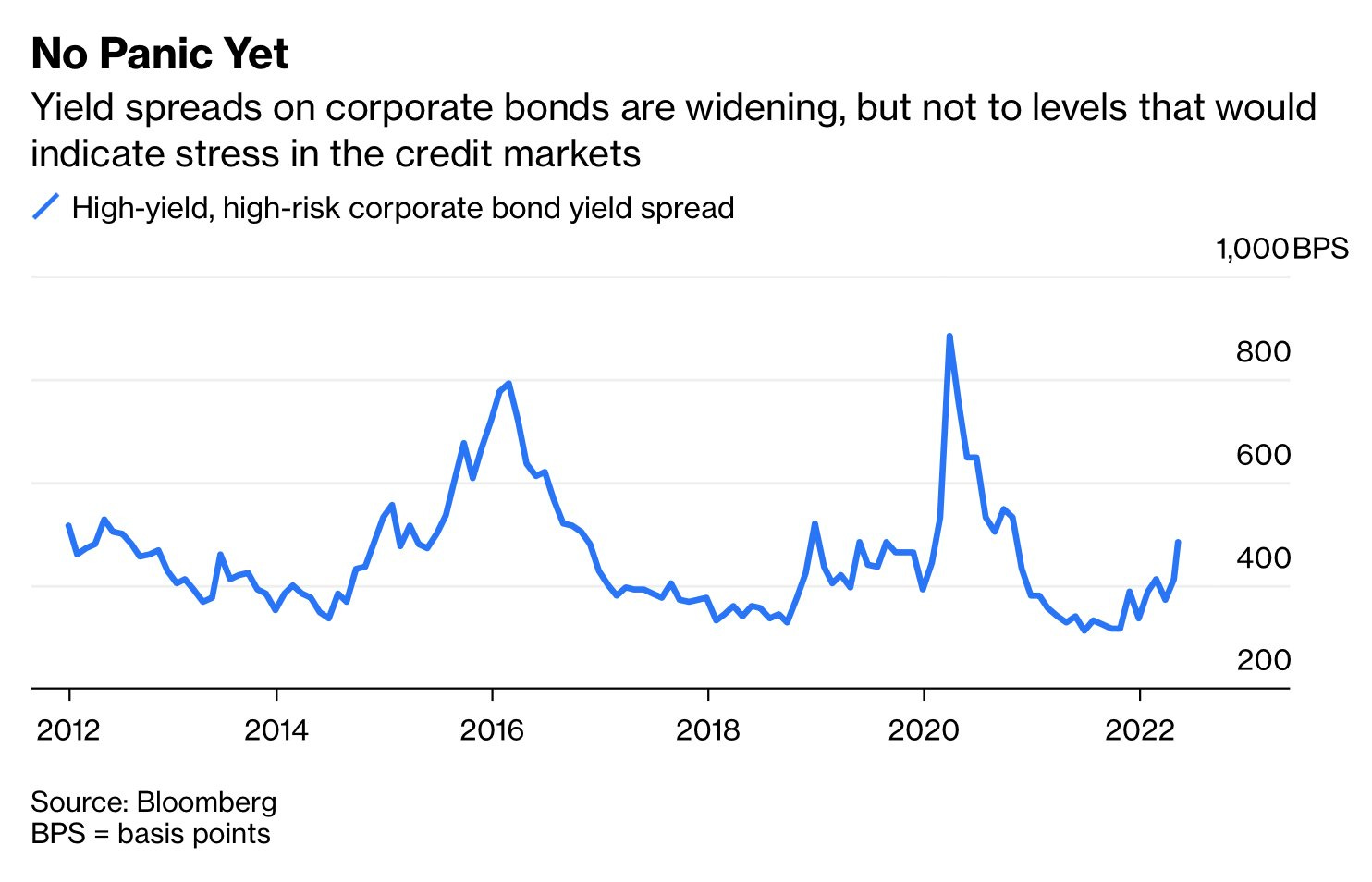

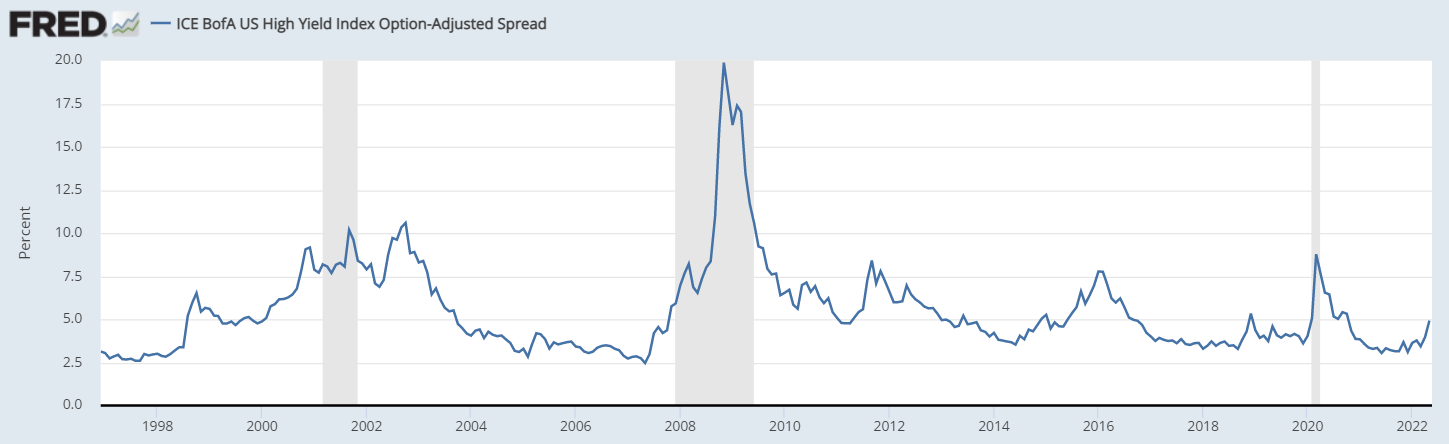

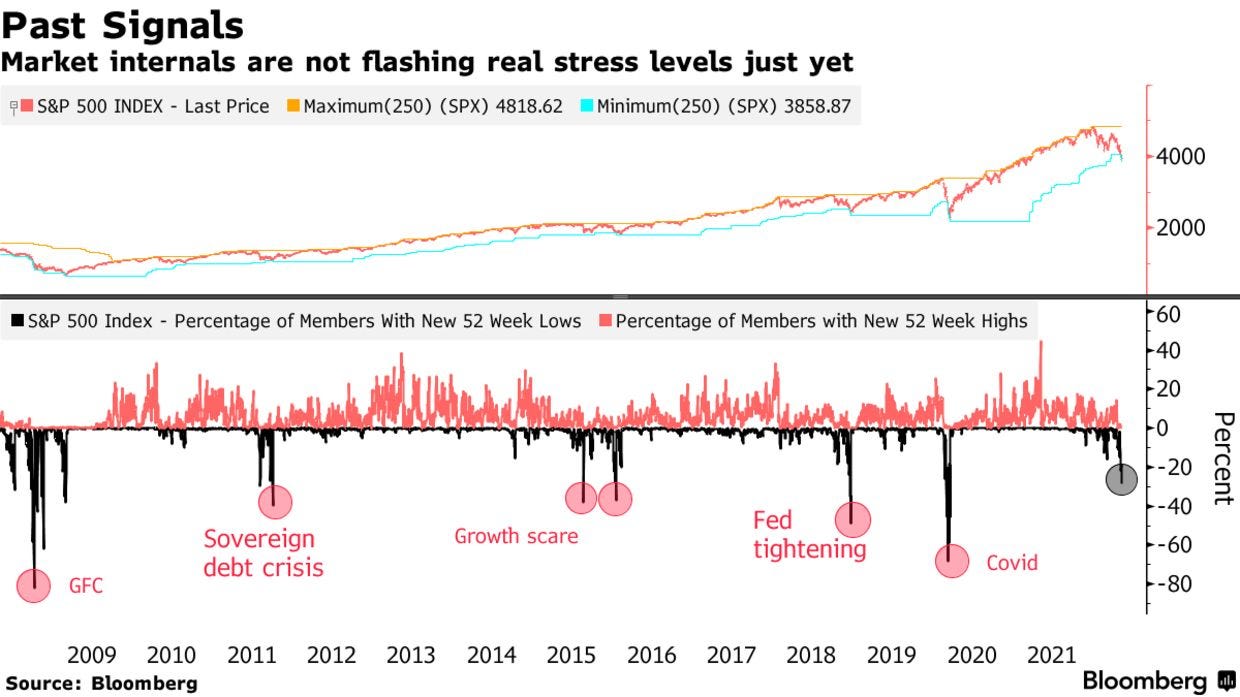

1: Treasury markets may be near March 2020 conditions (chart 1 shows declining depth of Treasury market), but there’s still a way to go before credit spreads reach ‘crisis’ levels (chart 2 and chart 3). Also, the equity market decline appears orderly (chart 4), as the number of S&P 500 constituents hitting 52 week lows is only about 30% (vs. 80% during the Global Financial Crisis or 70% during the Covid crash).

Seems contradictory, doesn’t it? The ‘risk free’ asset market is approaching stressed March 2020 levels, yet credit markets and risk assets remain orderly?!?

This makes me think two things:

Treasuries are likely suffering from a withdrawal of funding, possibly by the Fed and foreign entities. This makes intuitive sense, as the Fed is tightening monetary conditions and China is buying cheap Russian oil using Yuan (as opposed to on the open market in US dollars), requiring fewer dollar-denominated assets.

Investors have not yet capitulated.

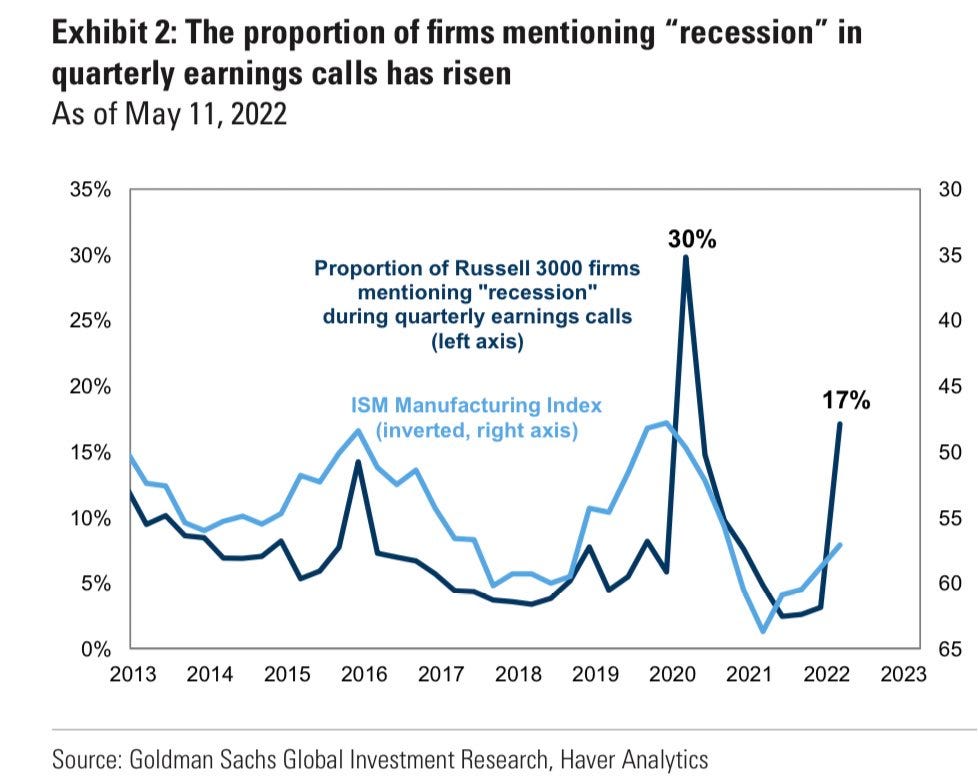

2: Recession talk (mentions during quarterly earnings calls + searches on Google) is quickly becoming mainstream. In my experience, by the time lots of people are talking about recession it has become a self-fulfilling prophecy. When people anticipate a recession, they slow spending, investment and hiring, thus contributing to the recession’s actualization.

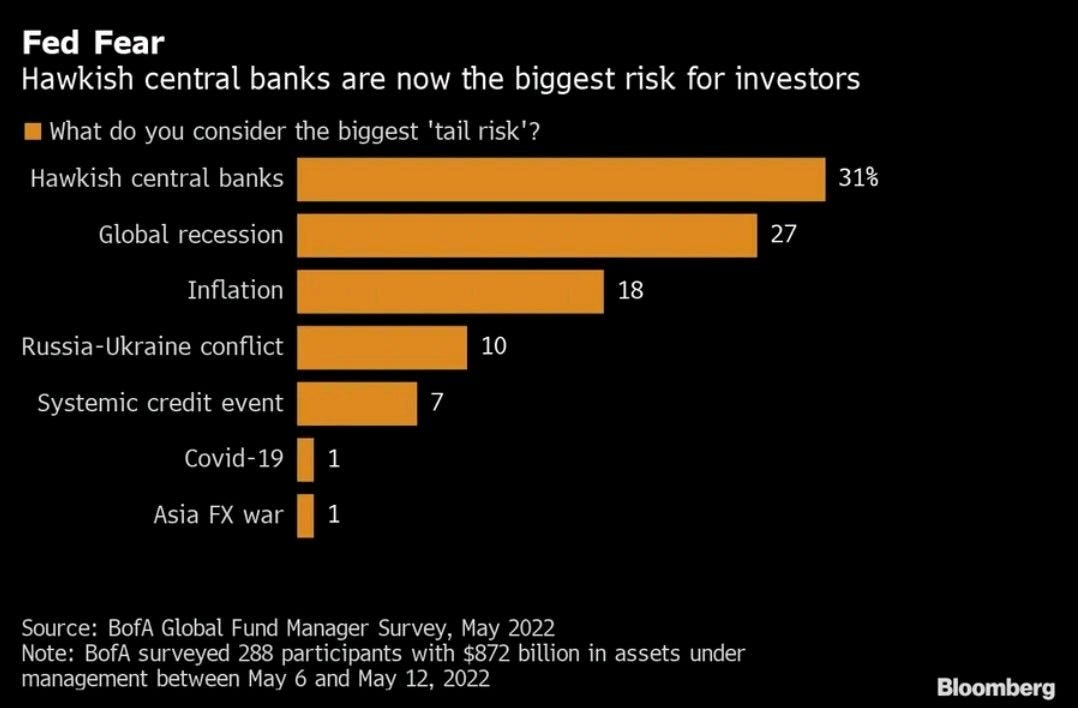

The things people are most worried about - central bank tightening and recession - are quickly becoming a reality.

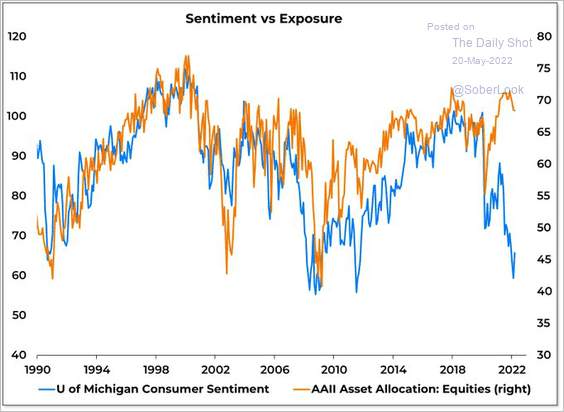

Consumer sentiment (U of Michigan Sentiment) echoes this, approaching Global Financial Crisis lows. Despite this, asset allocations remain fairly bullish. I expect that allocations follow sentiment, with investors continuing to withdraw from equities.

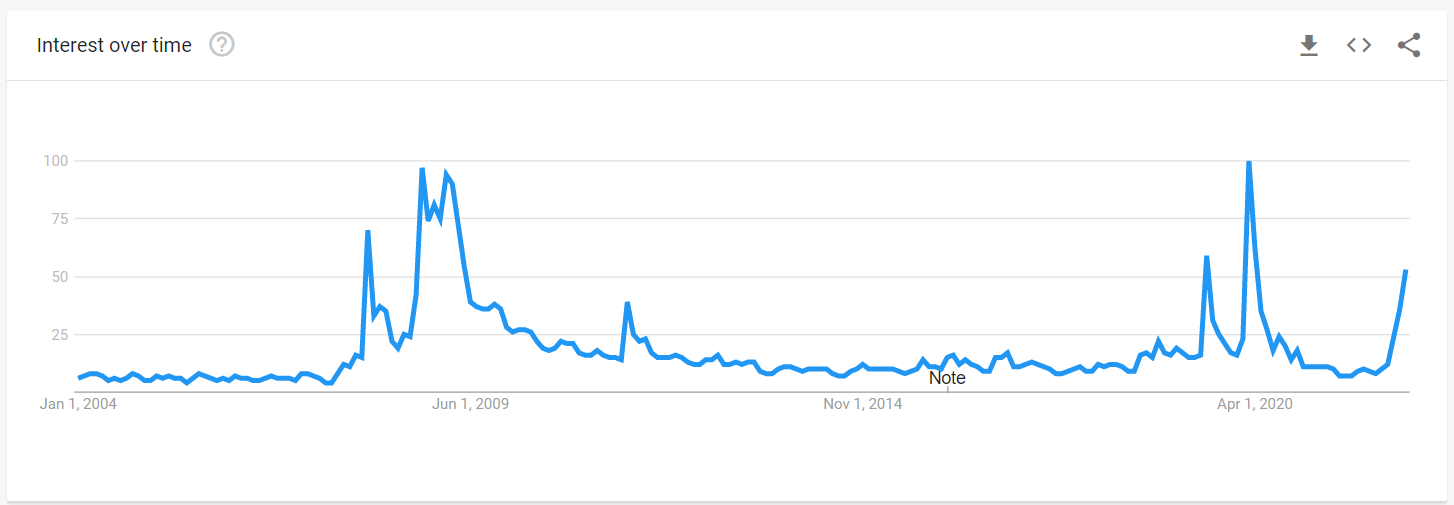

Google Trends’ worldwide interest in the term “recession”.

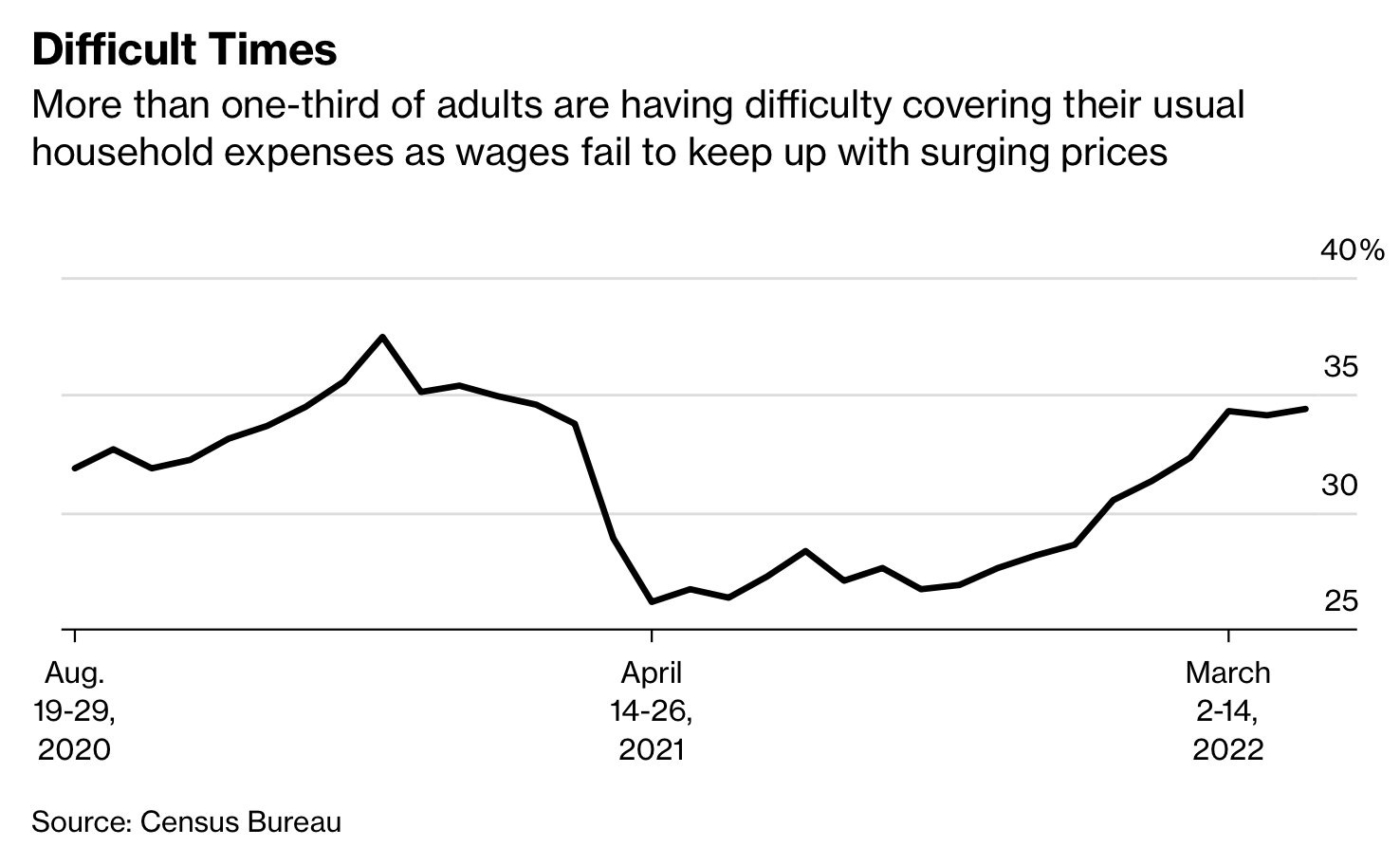

Declining sentiment is brought on by a combination of inflation and war. The inflationary drag is already taking a toll on spending. Over the past month alone, the proportion of people experiencing financial difficulty has risen by almost 10 percentage points. In fact, people are equating today’s difficulty with that of peak-Covid when the unemployment rate hit Great Depression levels.

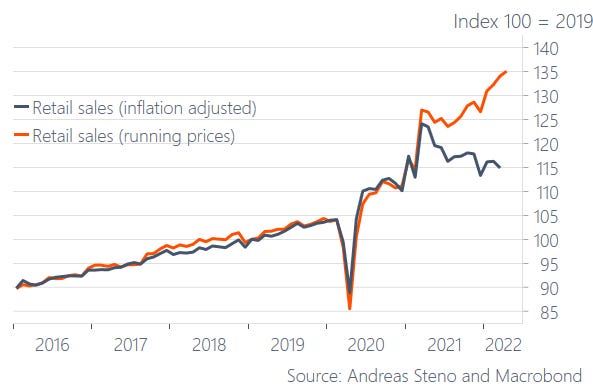

Individual financial difficulty is directly showing up in the real (inflation adjusted) spending data. Real retail sales is moving sideways or declining (depending on your starting reference point). Last week, the market puked on reports on a damaged consumer.

All this data tells me things are going to get worse.