The Resurrection of Paul Volcker

The Resurrection of Paul Volcker

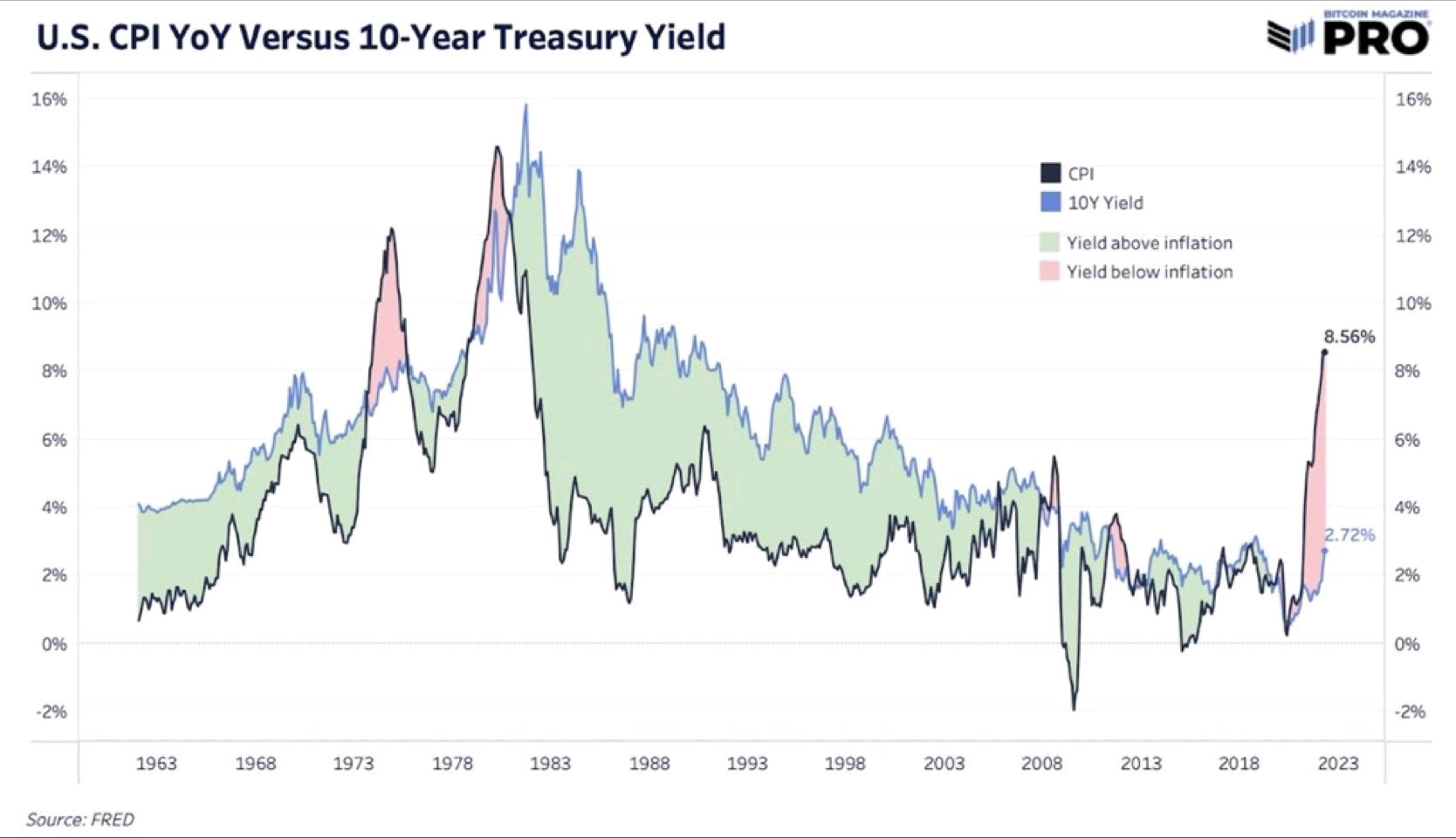

Today's inflation vs 1974 and 1980

1: The recent lockdowns throughout China are reigniting the process that led to supply chain issues throughout the world. The number of idle ships in Shanghai has skyrocketed over the past few weeks. This means more shipping delays, missing parts and sparse shelves. In other words, higher prices.

It’s one thing after another with this inflation problem. Covid, war, lockdowns, more war. And longer-term, a shortage of workers - as working age populations decline - could create upward pressure on wages (and prices). (Note that some argue that the long-term demographic situation is actually deflationary. This goes to show, behind the suits and the veneer of expertise analysts are really just giving their best educated guesses. There’s no playbook for this stuff.)

2: At the start of 2022 bond durations were high relative to history. Why? Because yields were so low - bond durations rise inversely to yields and coupons. In other words, the bond market was especially exposed to changes in interest rates, which have roughly doubled YTD 2022. The rate of change is extreme, causing double-digit declines for bonds.

Although the current decline is a historical anomaly, it is possible the worst is not behind us. The second chart below shows the 10yr US Treasury yield relative to CPI throughout history - today, the gap is immense. Only twice have real yields (nominal yields less inflation) been this negative - around 1974 and 1980. Both periods coincided with significant equity bear markets (third chart).

Note that during the 1974-ish period, negative real yields were resolved by a significant drop in inflation while bond yields only modestly drifted higher. In this case, the price shock likely kneecapped aggregate demand. In contrast, negative real yields during the 1980-ish periods were resolved by uber-aggressive Fed policy, led by former Fed chair Paul Volcker.

Today, the gap between yields and inflation could be narrowed in two ways: 1) rising prices could destroy aggregate demand, thus dragging inflation back to earth or 2) aggressive Fed policy tightening could reduce credit growth pushing the economy off a cliff, again destroying aggregate demand and lowering inflation.

My guess is there’s so much pent up demand and excess savings that consumers aren’t immediately cutting back and are willing to accept (for now) higher prices. Moreover, wage gains are softening the blow. While this might sound like it all balances out, it doesn’t as wage gains tend to lag. Worse, inflation could become endemic due to a price-wage spiral.

Therefore, the resolution is disproportionately in the Fed’s court. Unfortunately, the Fed is FAR behind the curve. It is likely that during this game of catch-up the Fed increases rates too fast and too far for the economy to bear, as it has many times throughout history (both accidentally and purposefully).

We may be witnessing the resurrection of Volcker policy.

Interesting. I see Volcker's name come up now a lot. Do you have any idea what rate-rising environment in Canada will do to housing prices here? I'm thinking of my parents time, when they bought a house for 107K in Stoney Creek with a 10% mortgage. They bought, by the way, because they had watched the price of that house rise from about 30K a decade earlier to 149K and then back down.